Page 41 - BAM ONE REPORT 2565 (ENGLISH VERSION)

P. 41

35

Form 56-1 One Report 2022

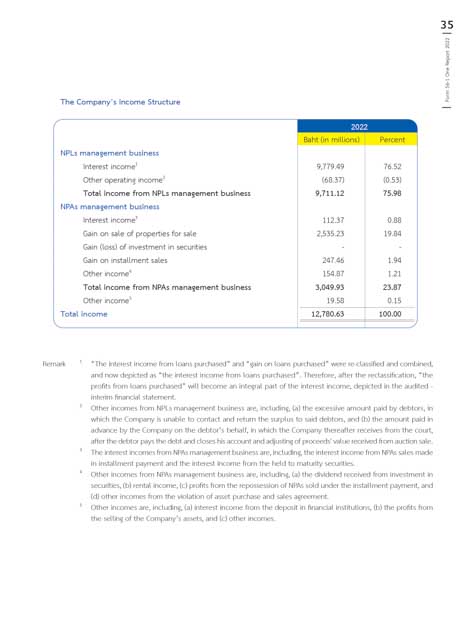

The Company’s Income Structure

2022

Baht (in millions) Percent

NPLs management business

Interest income 9,779.49 76.52

1

Other operating income 2 (68.37) (0.53)

Total income from NPLs management business 9,711.12 75.98

NPAs management business

Interest income 3 112.37 0.88

Gain on sale of properties for sale 2,535.23 19.84

Gain (loss) of investment in securities - -

Gain on installment sales 247.46 1.94

Other income 4 154.87 1.21

Total income from NPAs management business 3,049.93 23.87

Other income 5 19.58 0.15

Total income 12,780.63 100.00

Remark 1 “The interest income from loans purchased” and “gain on loans purchased” were re-classified and combined,

and now depicted as “the interest income from loans purchased”. Therefore, after the reclassification, “the

profits from loans purchased” will become an integral part of the interest income, depicted in the audited -

interim financial statement.

2 Other incomes from NPLs management business are, including, (a) the excessive amount paid by debtors, in

which the Company is unable to contact and return the surplus to said debtors, and (b) the amount paid in

advance by the Company on the debtor’s behalf, in which the Company thereafter receives from the court,

after the debtor pays the debt and closes his account and adjusting of proceeds' value received from auction sale.

3 The interest incomes from NPAs management business are, including, the interest income from NPAs sales made

in installment payment and the interest income from the held to maturity securities.

4 Other incomes from NPAs management business are, including, (a) the dividend received from investment in

securities, (b) rental income, (c) profits from the repossession of NPAs sold under the installment payment, and

(d) other incomes from the violation of asset purchase and sales agreement.

5 Other income are (a) intere income fr the de financia (b) the profi from

the selling of the Company’s assets, and (c) other incomes.