Page 217 - E-BOOK

P. 217

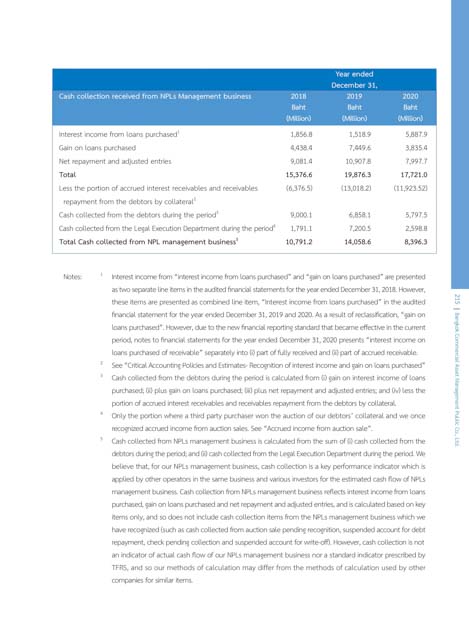

Year ended

December 31,

Cash collection received from NPLs Management business 2018 2019 2020

Baht Baht Baht

(Million) (Million) (Million)

1

Interest income from loans purchased 1,856.8 1,518.9 5,887.9

Gain on loans purchased 4,438.4 7,449.6 3,835.4

Net repayment and adjusted entries 9,081.4 10,907.8 7,997.7

Total 15,376.6 19,876.3 17,721.0

Less the portion of accrued interest receivables and receivables (6,376.5) (13,018.2) (11,923.52)

repayment from the debtors by collateral 2

3

Cash collected from the debtors during the period 9,000.1 6,858.1 5,797.5

Cash collected from the Legal Execution Department during the period 4 1,791.1 7,200.5 2,598.8

Total Cash collected from NPL management business 10,791.2 14,058.6 8,396.3

5

Notes: 1 Interest income from “interest income from loans purchased” and “gain on loans purchased” are presented

as two separate line items in the audited financial statements for the year ended December 31, 2018. However,

these items are presented as combined line item, “Interest income from loans purchased” in the audited 215

financial statement for the year ended December 31, 2019 and 2020. As a result of reclassification, “gain on

loans purchased”. However, due to the new financial reporting standard that became effective in the current

period, notes to financial statements for the year ended December 31, 2020 presents “interest income on

loans purchased of receivable” separately into (i) part of fully received and (ii) part of accrued receivable.

2 See “Critical Accounting Policies and Estimates- Recognition of interest income and gain on loans purchased”

3 Cash collected from the debtors during the period is calculated from (i) gain on interest income of loans Bangkok Commercial Asset Management Public Co., Ltd.

purchased; (ii) plus gain on loans purchased; (iii) plus net repayment and adjusted entries; and (iv) less the

portion of accrued interest receivables and receivables repayment from the debtors by collateral.

4 Only the portion where a third party purchaser won the auction of our debtors’ collateral and we once

recognized accrued income from auction sales. See “Accrued income from auction sale”.

5 Cash collected from NPLs management business is calculated from the sum of (i) cash collected from the

debtors during the period; and (ii) cash collected from the Legal Execution Department during the period. We

believe that, for our NPLs management business, cash collection is a key performance indicator which is

applied by other operators in the same business and various investors for the estimated cash flow of NPLs

management business. Cash collection from NPLs management business reflects interest income from loans

purchased, gain on loans purchased and net repayment and adjusted entries, and is calculated based on key

items only, and so does not include cash collection items from the NPLs management business which we

have recognized (such as cash collected from auction sale pending recognition, suspended account for debt

repayment, check pending collection and suspended account for write-off). However, cash collection is not

an indicator of actual cash flow of our NPLs management business nor a standard indicator prescribed by

TFRS, and so our methods of calculation may differ from the methods of calculation used by other

companies for similar items.