Page 52 - E-BOOK

P. 52

* These numbers are calculated based on the latest appraised price provided by the Appraisal

Committee (even for the case where there are more than 3 years of appraised prices available). On

the other hand, if the collaterals had been auctioned and bought, the purchased price after the

estimated expenses will be used for the calculation instead. The value of the collaterals will be

based on the appraised price first, before considering the debt obligation under the accrual basis

that the Company has with debtors, and before considering of the underlying collateral.

** These numbers are calculated by using the value of collaterals after the discount, specified under

BOT’s provision. The value of collaterals will not be used for the case where there are more than 3

years of appraised prices available, after the approval date of the appraised prices. On the other

hand, if the collaterals had been auctioned and bought, the purchased price after the estimated

expenses will be used for the calculation instead. The value of the underlying collateral will be based

on the appraised price first, before considering the debt obligation under the accrual basis that the

Company has with debtors, and before considering of the underlying collateral.

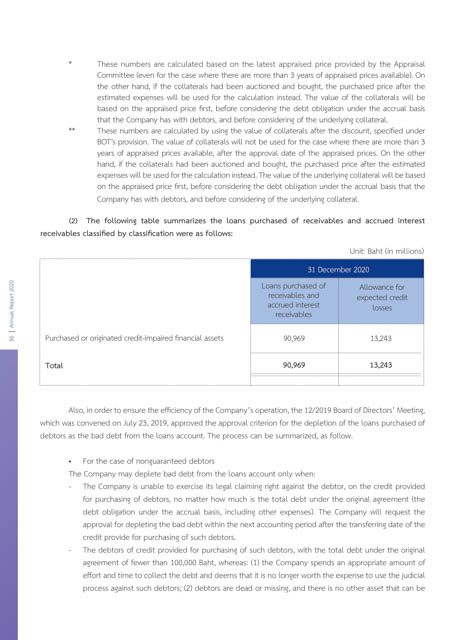

(2) The following table summarizes the loans purchased of receivables and accrued interest

receivables classified by classification were as follows:

Unit: Baht (in millions)

31 December 2020

Loans purchased of Allowance for

receivables and expected credit

accrued interest losses

receivables

50 Purchased or originated credit-impaired financial assets 90,969 13,243

Total 90,969 13,243

Also, in order to ensure the efficiency of the Company’s operation, the 12/2019 Board of Directors’ Meeting,

which was convened on July 23, 2019, approved the approval criterion for the depletion of the loans purchased of

debtors as the bad debt from the loans account. The process can be summarized, as follow.

• For the case of nonguaranteed debtors

The Company may deplete bad debt from the loans account only when:

- The Company is unable to exercise its legal claiming right against the debtor, on the credit provided

for purchasing of debtors, no matter how much is the total debt under the original agreement (the

debt obligation under the accrual basis, including other expenses). The Company will request the

approval for depleting the bad debt within the next accounting period after the transferring date of the

credit provide for purchasing of such debtors.

- The debtors of credit provided for purchasing of such debtors, with the total debt under the original

agreement of fewer than 100,000 Baht, whereas: (1) the Company spends an appropriate amount of

effort and time to collect the debt and deems that it is no longer worth the expense to use the judicial

process against such debtors; (2) debtors are dead or missing, and there is no other asset that can be