Page 320 - BAM ONE REPORT 2565 (ENGLISH VERSION)

P. 320

314

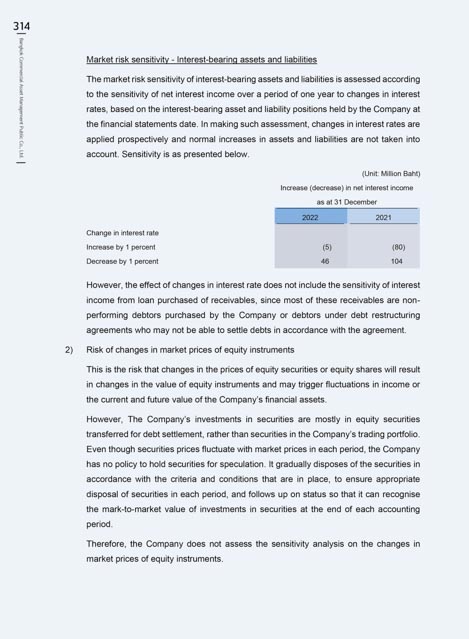

Market risk sensitivity - Interest-bearing assets and liabilities

The market risk sensitivity of interest-bearing assets and liabilities is assessed according

to the sensitivity of net interest income over a period of one year to changes in interest

rates, based on the interest-bearing asset and liability positions held by the Company at

the financial statements date. In making such assessment, changes in interest rates are

applied prospectively and normal increases in assets and liabilities are not taken into

account. Sensitivity is as presented below.

Bangkok Commercial Asset Management Public Co., Ltd.

(Unit: Million Baht)

Increase (decrease) in net interest income

as at 31 December

2022 2021

Change in interest rate

Increase by 1 percent (5) (80)

Decrease by 1 percent 46 104

However, the effect of changes in interest rate does not include the sensitivity of interest

income from loan purchased of receivables, since most of these receivables are non-

performing debtors purchased by the Company or debtors under debt restructuring

agreements who may not be able to settle debts in accordance with the agreement.

2) Risk of changes in market prices of equity instruments

This is the risk that changes in the prices of equity securities or equity shares will result

in changes in the value of equity instruments and may trigger fluctuations in income or

the current and future value of the Company’s financial assets.

However, The Company’s investments in securities are mostly in equity securities

transferred for debt settlement, rather than securities in the Company’s trading portfolio.

Even though securities prices fluctuate with market prices in each period, the Company

has no policy to hold securities for speculation. It gradually disposes of the securities in

accordance with the criteria and conditions that are in place, to ensure appropriate

disposal of securities in each period, and follows up on status so that it can recognise

the mark-to-market value of investments in securities at the end of each accounting

period.

Therefore, the Company does not assess the sensitivity analysis on the changes in

market prices of equity instruments.

66