Page 317 - BAM ONE REPORT 2565 (ENGLISH VERSION)

P. 317

311

Form 56-1 One Report 2022

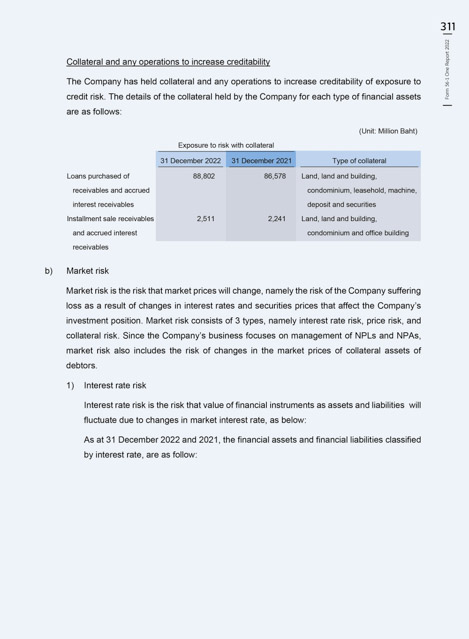

Collateral and any operations to increase creditability

The Company has held collateral and any operations to increase creditability of exposure to

credit risk. The details of the collateral held by the Company for each type of financial assets

are as follows:

(Unit: Million Baht)

Exposure to risk with collateral

31 December 2022 31 December 2021 Type of collateral

Loans purchased of 88,802 86,578 Land, land and building,

receivables and accrued condominium, leasehold, machine,

interest receivables deposit and securities

Installment sale receivables 2,511 2,241 Land, land and building,

and accrued interest condominium and office building

receivables

b) Market risk

Market risk is the risk that market prices will change, namely the risk of the Company suffering

loss as a result of changes in interest rates and securities prices that affect the Company’s

investment position. Market risk consists of 3 types, namely interest rate risk, price risk, and

collateral risk. Since the Company’s business focuses on management of NPLs and NPAs,

market risk also includes the risk of changes in the market prices of collateral assets of

debtors.

1) Interest rate risk

Interest rate risk is the risk that value of financial instruments as assets and liabilities will

fluctuate due to changes in market interest rate, as below:

As at 31 December 2022 and 2021, the financial assets and financial liabilities classified

by interest rate, are as follow:

63