Page 210 - E-BOOK

P. 210

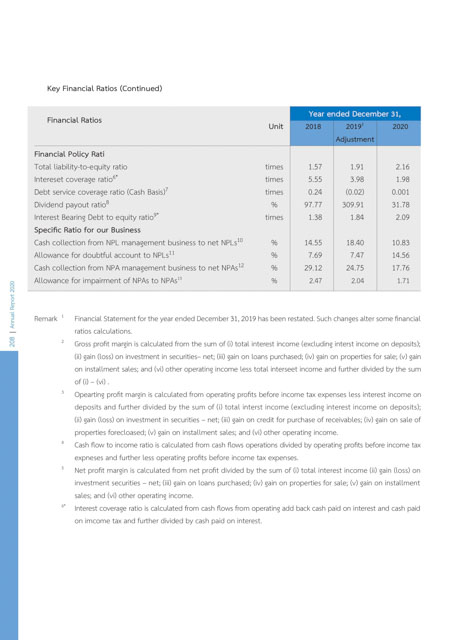

Key Financial Ratios (Continued)

Year ended December 31,

Financial Ratios

Unit 2018 2019 1 2020

Adjustment

Financial Policy Rati

Total liability-to-equity ratio times 1.57 1.91 2.16

Intereset coverage ratio 6* times 5.55 3.98 1.98

Debt service coverage ratio (Cash Basis) 7 times 0.24 (0.02) 0.001

Dividend payout ratio 8 % 97.77 309.91 31.78

Interest Bearing Debt to equity ratio 9* times 1.38 1.84 2.09

Specific Ratio for our Business

Cash collection from NPL management business to net NPLs 10 % 14.55 18.40 10.83

Allowance for doubtful account to NPLs 11 % 7.69 7.47 14.56

Cash collection from NPA management business to net NPAs 12 % 29.12 24.75 17.76

Allowance for impairment of NPAs to NPAs 13 % 2.47 2.04 1.71

Annual Report 2020 Remark Financial Statement for the year ended December 31, 2019 has been restated. Such changes alter some financial

1

ratios calculations.

208 2 Gross profit margin is calculated from the sum of (i) total interest income (excluding interst income on deposits);

(ii) gain (loss) on investment in securities– net; (iii) gain on loans purchased; (iv) gain on properties for sale; (v) gain

on installment sales; and (vi) other operating income less total interseet income and further divided by the sum

of (i) – (vi) .

Opearting profit margin is calculated from operating profits before income tax expenses less interest income on

3

deposits and further divided by the sum of (i) total interst income (excluding interest income on deposits);

(ii) gain (loss) on investment in securities – net; (iii) gain on credit for purchase of receivables; (iv) gain on sale of

properties forecloased; (v) gain on installment sales; and (vi) other operating income.

Cash flow to income ratio is calculated from cash flows operations divided by operating profits before income tax

4

expneses and further less operating profits before income tax expenses.

Net profit margin is calculated from net profit divided by the sum of (i) total interest income (ii) gain (loss) on

5

investment securities – net; (iii) gain on loans purchased; (iv) gain on properties for sale; (v) gain on installment

sales; and (vi) other operating income.

Interest coverage ratio is calculated from cash flows from operating add back cash paid on interest and cash paid

6*

on imcome tax and further divided by cash paid on interest.