Page 49 - BAM ONE REPORT 2565 (ENGLISH VERSION)

P. 49

43

Form 56-1 One Report 2022

Moreover, the Company constantly monitors the outcome of its investment, which is a function of the Assets

and liabilities Management Committee, who, in turn, report the outcome to the Executive Committee and/ or the

Board of Directors, for the result of the Company’s investment portfolios. The information provided herein will be

used as factors for the consideration of acquiring other investment portfolios in the future.

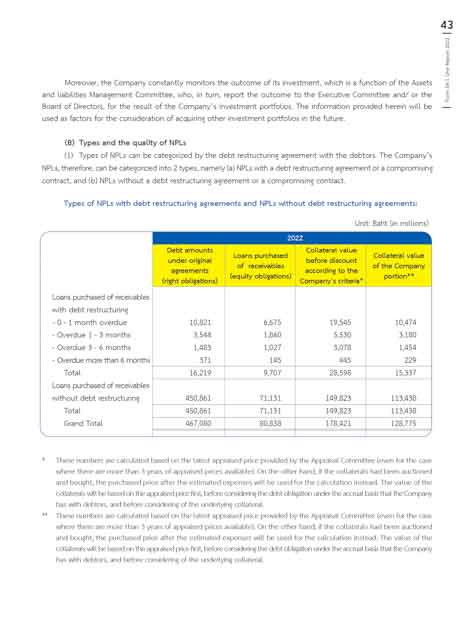

(B) Types and the quality of NPLs

(1) Types of NPLs can be categorized by the debt restructuring agreement with the debtors. The Company’s

NPLs, therefore, can be categorized into 2 types, namely (a) NPLs with a debt restructuring agreement or a compromising

contract, and (b) NPLs without a debt restructuring agreement or a compromising contract.

Types of NPLs with debt restructuring agreements and NPLs without debt restructuring agreements:

Unit: Baht (in millions)

2022

Debt amounts Collateral value

under original Loans purchased before discount Collateral value

agreements of receivables according to the of the Company

(right obligations) (equity obligations) Company’s criteria* portion**

Loans purchased of receivables

with debt restructuring

- 0 - 1 month overdue 10,821 6,675 19,545 10,474

- Overdue 1 - 3 months 3,544 1,860 5,530 3,180

- Overdue 3 - 6 months 1,483 1,027 3,078 1,454

- Overdue more than 6 months 371 145 445 229

Total 16,219 9,707 28,598 15,337

Loans purchased of receivables

without debt restructuring 450,861 71,131 149,823 113,438

Total 450,861 71,131 149,823 113,438

Grand Total 467,080 80,838 178,421 128,775

* These numbers are calculated based on the latest appraised price provided by the Appraisal Committee (even for the case

where there are more than 3 years of appraised prices available). On the other hand, if the collaterals had been auctioned

and bought, the purchased price after the estimated expenses will be used for the calculation instead. The value of the

collaterals will be based on the appraised price first, before considering the debt obligation under the accrual basis that the Company

has with debtors, and before considering of the underlying collateral.

** These numbers are calculated based on the latest appraised price provided by the Appraisal Committee (even for the case

where there are more than 3 years of appraised prices available). On the other hand, if the collaterals had been auctioned

and bought, the purchased price after the estimated expenses will be used for the calculation instead. The value of the

collaterals will be based on the appraised price first, before considering the debt obligation under the accrual basis that the Company

has with debtors, and before considering of the underlying collateral.